Where Nature Meets Climate - a guide to the complex world of climate mitigation and nature positive action

Where Nature Meets Climate - a guide to the complex world of climate mitigation and nature positive action

Episode 1. The Overview - From Article 6, to SBTi, to TNFD and many in between, let's dive into how these initiatives are driving natural climate solutions and nature-positive action.

Over the last couple of months I’ve been wading through the plethora of initiatives with the ambition of stimulating high-integrity voluntary climate action and action towards protecting and restoring nature. And, with the nudging of a few friends, I figured sharing my learnings and analysis might help others better understand the current state, challenges and opportunities that these initiatives bring. This is the first of many “episodes” that I hope anyone in the nature conservation/restoration, carbon markets, naturetech and nature/carbon finance space will find helpful to navigate the complexity. Welcome to the first episode of the Where Nature Meets Climate series - The Overview.

Today, we’ll take a look at seven initiatives currently driving global voluntary climate action and nature positive activities, the initiatives that are looking to build confidence and trust in those frameworks and emerging initiatives that have significant potential to catalyze new action. I could have written seven different posts, one on each initiative, but I think one of the most interesting aspects of these initiatives is how they are working together (or in some ways working against each other) and what are the implications of that overlap for the climate and nature.

Article 6.4 of the Paris Climate Accord (A6.4)

Science Based Targets Initiative Corporates Net-zero Standard (SBTi-CNS)

Science Based Targets Initiative Beyond Value Chain Mitigation (SBTi-BVCM)

Integrity Council on Voluntary Carbon Markets (ICVCM)

Voluntary Carbon Markets Integrity Initiative (VCMI)

Science Based Targets for Nature (SBTN)

Taskforce for Nature-related Financial Disclosures (TNFD)

For each of these initiatives, we’ll cover the following:

Intention: What is the purpose of the initiative and who is managing it?

Status: What is the current state of readiness/deployment of the initiative?

Impact: What effect is the initiative currently having or what is the impact it could have if it is not yet being implemented? Remember, we’ll be looking at impact specifically as it relates to catalyzing natural climate solutions and nature positive outcomes.

Overlap: Where does the initiative have overlap, whether in a good way or a bad way with other initiatives and what are the implications?

Opportunity: My two cents on how the initiative could shift/evolve to itself achieve better outcomes or work more efficiently with other initiatives

WARNING: This may get a bit wonky at times, but embrace the wonk and I think you’ll find navigating this space not nearly as intimidating 🙂.

Science Based Targets Initiative Corporate Net-zero Standard (SBTi-CNS)

Let’s start with SBTi-CNS because it is the most well known and established of all seven initiatives.

Intention: Science-based targets for climate were created to provide a clearly-defined pathway for companies and financial institutions to reduce greenhouse gas (GHG) emissions in line with what the latest climate science says is necessary to meet the goals of the Paris Agreement – limiting global warming to 1.5°C above pre-industrial levels. “By guiding companies in science-based target setting, we enable them to tackle global warming while seizing the benefits and boosting their competitiveness in the transition to a zero-carbon economy.” SBTi-CNS is exclusively focused on carbon accounting and driving corporate voluntary climate action.

Status: Active since 2015

Impact: SBTi-CNS has focused on driving decarbonization and has a clear position on offsetting: “The SBTi requires that companies set targets based on emission reductions through direct action within their own boundaries or their value chains. Offsets are only considered to be an option for companies wanting to finance additional emission reductions beyond their science-based target (SBT) or net-zero target.” SBTi has gotten significant traction and has been the main driver of demand for the voluntary carbon market. But there have been some critiques of their recent shift to remove the use of offsets to meet a netzero ambition.

The critique of this approach is that corporates will (1) not be able to meet their net-zero targets because the cost of decarbonizing is too high, (2) lead to corporates not contributing to climate mitigation and resilience in places that are outside of their supply chain, but experiencing the greatest impacts of climate change (much of the global south), and results in less support for natural climate solutions as much of those fall outside of corporate value chains.

Overlap: Because of these critiques, SBTi launched the Beyond Value Chain Mitigation guidance, which is essentially their way of saying corporates should take climate action (like purchasing carbon credits) as a “contribution” to climate mitigation outside of their core operations while focusing on decarbonizing within their value chain. And as SBTi realized that the health of the planet goes beyond carbon concentration in the atmosphere, they launched the Science-based Targets for Nature which aims to drive corporate voluntary action to protect and restore nature (more to come on these later).

Opportunity/Analysis: My assessment is that SBTi has essentially created a “harm” ledger, which is the total emissions that corporate is responsible for (SBTi-CNS), and a “doing good” ledger which is the climate mitigation the corporate has funded (SBTi-BVCM). I am actually ok with having two ledgers. Whether you combine the two to make a claim (like carbon neutral) or you keep them separate is a marketing and branding decision, but ultimately it is the totals in each of those two ledgers that matter. But, there is a way we can keep it simple, stick with a net-zero structure and allow for offsets to play a critical role - what’s needed is a shift in the accounting, going from a static to a dynamic system.

Alicia Seiger et al. 2022 said it best in a working paper released last November, “Few carbon offset strategies match the certainty and duration of emissions liabilities. As a result, offsets have been shunned by leading standards bodies like the Science Based Targets Initiative (SBTI), thereby stifling needed investment in protecting natural capital and technology-driven sequestration. She and her co-authors propose an Emissions Liability Management system. They cover the approach in detail in the working paper, but for the purposes of this discussion, it is essentially a dynamic accounting system where a carbon removal or avoided emissions credit can only be used for a claim as long as it is still additional and intact (ie doesn’t experience a reversal event like a wildfire). And if that credit found to have been a part of a reversal event, then it needs to be replaced by the entity using that credit for a claim. This overcomes the challenge of a static system, whereby there are significant risks that credits retired to meet net-zero commitments, could later experience a reversal.

One key update to existing systems that I believe would be required to implement an ELM system (and should be required for current systems anyways) is for land-based credits to have a unique geo-tag representing the location where that credit was produced. I’m of the opinion that end buyers should be responsible for the costs of monitoring for removals or avoided emissions from deforestation and degradation as long as they are using that credit for a climate mitigation claim. And that credit should be monitored for reversals as long as it is being used for a claim. If 10% of a forest is burned in a fire and there aren’t geo-tags, but multiple buyers have purchased credits from that project, which credits are officially reversed and need to be replaced? We need a geo-tag so that entities using that credit for a climate mitigation claim will know if their credit needs to be replaced due to a reversal event. I believe we are at the stage with remote sensing technologies and digital ledgers that this shouldn’t be too difficult to do (and will become cheaper over time). Potential implication: this could lead to credits within a project being valued higher if they have a lower reversal risk which could further complicate pricing/sales, but I’m of the opinion that this is necessary for long-term responsibility and ownership of reversals.

My recommendation to SBTi: don’t produce two different sets of guidance for corporates to follow, SBTi-CNS and SBTi-BVCM. Keep it all within SBTi-CNS and allow for offsets to be used as part of a net-zero commitment (while following the clear hierarchy and requirements within SBTI regarding decarbonization en route to net-zero to avoid a ‘license to pollute’ scenario) and institute an Emissions Liability Management system or similar system that incorporates dynamic accounting instead of static. And perhaps even create a larger ambition for corporates that want to go beyond net-zero and contribute to carbon drawdown above and beyond their historical emissions. My recommendation is based on the logic that the simpler we can keep guidance for corporates to follow and the fewer times we change the claims language, the more corporates that will take voluntary action.

One other key question of the decarbonization approach that includes insetting is that it is still unclear to me where robust rules exist for who is verifying corporate emissions and how transparent is this reporting? I’ll be the first to admit this is not my area of expertise, but if we are going to be highly critical of carbon credits and climate mitigation outside of value chains, I would hope we are being as critical of decarbonization and climate mitigation within value chains.

Science Based Targets Initiative Beyond Value Chain Mitigation (SBTi-BVCM)

Intention: “Guidance to support companies to go beyond their science-based targets by channeling additional climate finance towards mitigation activities outside of their value chains.” Essentially, here’s how you can contribute to climate mitigation in addition to decarbonizing your company.

Status: Currently undergoing a public consultation for key questions regarding the guidance that will inform the finalization of the first version of the guidance (likely late 2023).

Impact: It makes sense for corporates to contribute to climate mitigation outside of their value chains, especially given that decarbonization is a longer process and we want corporates to be sticking to a 1.5 degree pathway. SBTi-BVCM does open up the door for more corporate contributions to natural climate solutions which is welcome.

Overlap/Opportunity: Is it a mistake to be creating an additional set of guidance for corporates to follow? My sense is yes given that a dynamic accounting system such as the one I presented in the previous section would enable corporate decarbonization and contributions to climate mitigation to sit within a single program.

Integrity Council on Voluntary Carbon Markets (ICVCM)

Intention: The Integrity Council for the Voluntary Carbon Market (ICVCM) is an independent governance body for the voluntary carbon market. Think of ICVCM as the watchperson who watches the watchpeople in the voluntary market. The ICVCM Core Carbon Principles and Assessment Framework set the bar that all carbon certification entities (like Verra, Gold Standard, CAR, ACR, Plan Vivo, etc… need to meet in order to get ICVCM’s stamp of approval (the CCP Label). The ICVCM won’t be certifying individual projects, but will be certifying the standards that do certify individual projects. The ICVCM will also develop criteria and provide a CCP Label a “Category” basis, which they define as same project type, same crediting program, same version of the methodology and in some cases similar location. Note that the ICVCM is supply side focused and was created to ensure the integrity and quality of carbon credits. They do not make any suggestions as to the accounting structures or claims made using those credits.

Status: As of July 26th, 2023, the ICVCM has launched the initial version of it’s Core Carbon Principles and the Assessment Framework, as well as the Assessment Platform where certifying programs, like Verra, can apply for the CCP Label.

Impact: To be seen… the purpose of the ICVCM is to restore trust in carbon markets after significant critique of the integrity of the credits that were approved by the existing major crediting programs. I think it is necessary as an oversight body to provide one label that investors and buyers can trust. But the devil will be in the details and the extent to which the ICVCM can effectively govern the standards and resolve the issues that have historically existed. My personal opinion is that carbon markets and the rules that govern them naturally will be revised over time as we find blind spots that earlier regulators didn’t see and I welcome the work of the ICVCM to help all certifying programs level up their methodologies and their processes.

Overlap: Here’s where there are a couple of downsides. First is that certification programs will likely have to designate a significant amount of their already limited human resource to achieving the CCP approval which will further slow the certification of projects at a time where project certification is taking longer than ever. Second, I am conscious of the work within SBTi-BVCM and A6.4 to write new methodologies and again, I am hoping we don’t end up with multiple standards/oversight groups with corporates (and governments for that matter) further confused as to what to trust, not to mention the duplication of efforts.

Opportunity: My hope is two fold, (1) the ICVCM establishes itself as the global watchdog for any carbon crediting program, whether voluntary or compliance and it’s approach proves effective at ensuring the integrity and quality of outcomes leading to it’s label being the source of truth for credit integrity and (2) the SBTi-CNS and SBTi-BVCM both adapt the crediting programs and categories that have received ICVCM certification so that instead of focusing on the integrity of the climate mitigation outcome, SBTi can focus on the integrity of corporate decarbonization and the integrity of the overall accounting and the claim. And if I could add one more, if individual countries or even the UN decide to launch their own oversight and certification bodies, my hope is that they all use the same foundation (which could be the ICVCM) to both save them time and to ensure that programs between countries can be trusted and facilitate more seamless trading of credits between countries, whether through A6.4 or another mechanism.

Now what could the ICVCM mean for nature? There have been multiple nature-based projects, primarily REDD projects, that have been approved by existing carbon certifying programs that have been shown to not have had the climate mitigation impact that they claimed to have. Hopefully the establishment of the ICVCM will raise the bar across all certification programs and, combined with my suggestions above around dynamic accounting which addresses the permanence critique, increases demand side trust in nature-based credits and investments into those solutions.

Voluntary Carbon Markets Integrity Initiative (VCMI)

Intention: As it says on their website - “The Voluntary Carbon Markets Integrity Initiative (VCMI) is an international non-profit organization with a mission to enable high-integrity voluntary carbon markets (VCMs) that deliver real and additional benefits to the atmosphere, help protect nature, and accelerate the transition to ambitious, economy-wide climate policies and regulation.” The key difference between ICVCM and VCMI is that ICVCM is focused on the quality of the credits and the supply side of the equation, whereas VCMI is focused on the quality of the climate mitigation itself, the demand side of carbon markets.

Status: VCMI just released it’s Claims Code of Practice in July of 2023.

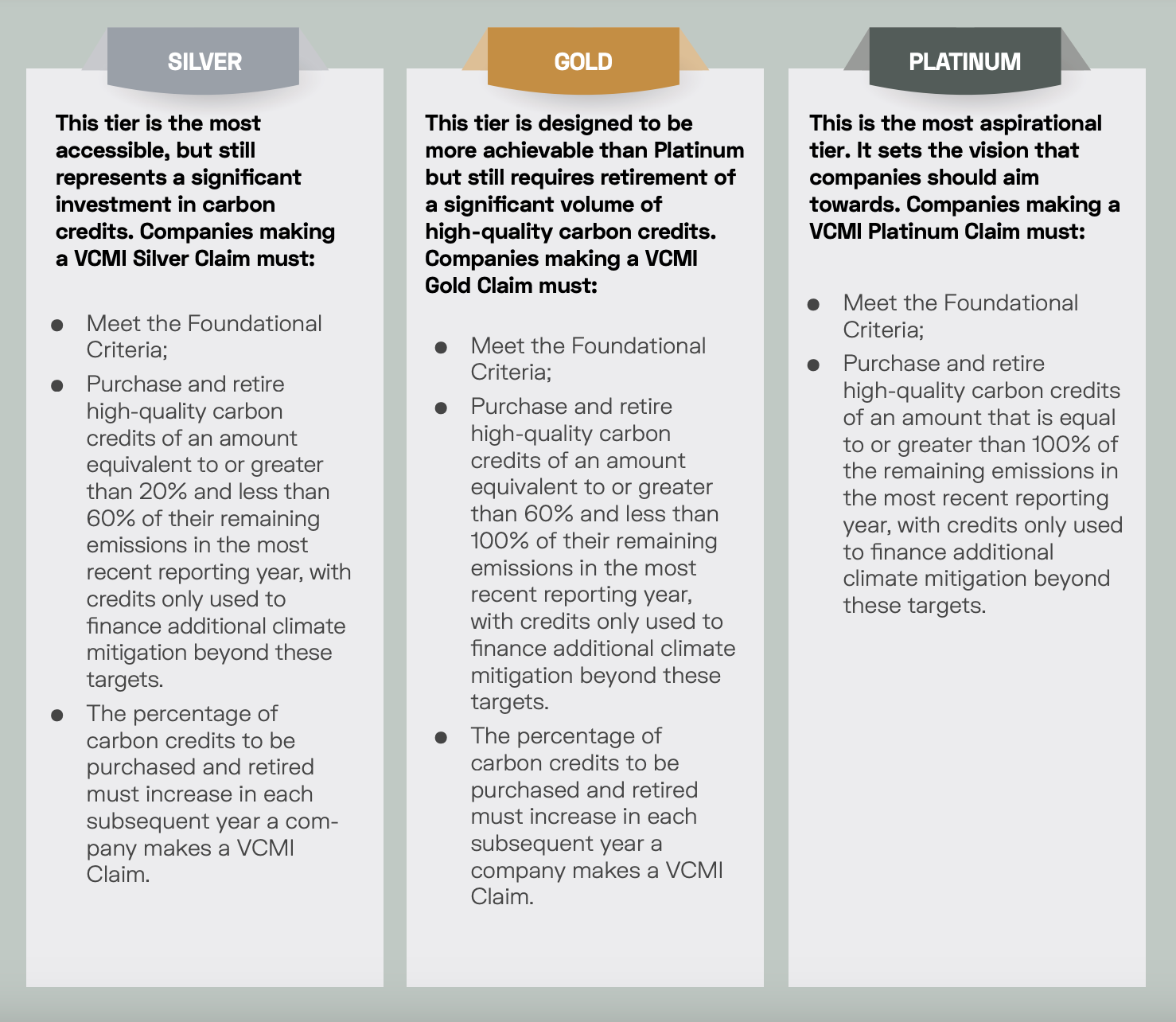

Impact: The Claims Code of Practice is a rulebook on credible use of high-quality carbon credits, and associated climate claims, that will accelerate climate action. As far as I understand it, the VCMI was largely created as a result of the criticism of the claims that corporates were making around “carbon neutral” or “carbon netzero” not being truthful. The Claims Code of Practice lays out four steps that a company must take in order to meet the Claims Code (as the ICVCM is the watchdog for carbon certifying programs, the VCMI is establishing itself as the watchdog for corporate claims).

It must first meet VCMI’s Foundational Criteria, which serve as the backbone of an ambitious and robust climate strategy; (Focused on clear commitment to reducing emissions first, see the details in the Claims Code pg. 6)

It must then select which VCMI Claim to make (Platinum, Gold or Silver);

To make the claim, the company must select carbon credits which meet stringent quality thresholds in line with the Integrity Council for Voluntary Carbon Markets (ICVCM) Core Carbon Principles (CCPs);

Finally, the company must disclose information to support its claim and conduct independent validation and assurance in line with the VCMI MRV and Assurance Framework (to be published in November 2023.)

Overlap: How is VCMI working with other initiatives? You can see above that VCMI is using the CCPs of the ICVCM as their carbon credit quality bar. How is it perhaps in conflict with other initiatives? This is where things get interesting. SBTi-CNS currently does not allow for carbon credits to be used as offsets to make a net-zero claim. VCMI instead implements three tiers of claims that allow for use of carbon credits but have a completely different claims language:

There’s a lot of discussion as to whether we should stray from net-zero claims language to get corporates to adopt a new claims language. Personally, I am not sure the silver, gold, platinum approach will have the same resonance with consumers which is the main driver of voluntary corporate climate action. But from nature’s perspective, the fact that VCMI does include the use of carbon credits within a climate mitigation claim makes it far more attractive than SBTi-CNS where almost all natural climate solution action (other than some insetting) has been pushed to SBTi Beyond Value Chain Mitigation.

Opportunity:

It’s quite valuable to have an entity that is looking under the hood at corporate climate claims and making sure their action can back up the claim. And I am in agreement with VCMI that carbon credits should be able to be used within a climate mitigation claim as long as the corporate is on a clear path towards decarbonizing aligned with the Paris Climate Accord. But I don’t think that moving away from net-zero and creating possibly more claims language (that might not be able to evolve with the industry as we’ve seen with LEED building certification) is the right move.

Here are a couple of ideas, maybe you agree with them, maybe you don’t, this is just to get some healthy discussion going! My sense is that SBTi-CNS to switch to a dynamic accounting system like the Emission Liability Management system and allow for carbon credits in reaching net-zero AND have VCMI be the oversight body on the climate mitigation claims and ICVCM be the oversight body on the integrity of the carbon credits used in those claims. With both of those groups working in partnership with SBTi and adopting a netzero structure that has dynamic accounting and allows for offsets, we can avoid needing to set up an additional standard, SBTi-BCVM. Instead we can create additional claims for corporates that go beyond net-zero to climate mitigation beyond their emissions that could be within or beyond their value chain.

Food for thought…

Article 6.4 of the Paris Climate Accord (A6.4)

Intention: Article 6.4 of the Paris Climate Accord laid the foundation for a new global carbon market overseen by a United Nations entity, referred to as the “Article 6.4 Supervisory Body” (6.4SB). The credits, known as A6.4ERs, can be bought by countries, companies, or even individuals. A6.4 is largely seen as v2 of the Clean Development Mechanism (CDM).

Status: According to Carbon Market Watch, it is unlikely any credits will be issued or traded until 2024 at the earliest. This system is overseen by the UN Supervisory Body mentioned above. A6.4ERs cannot be traded until this regulatory body and a centralized registry are in place. As of COP27, there were still ongoing negotiations around the core design of A6.4 and while there is hope that there will be full agreement at COP28 in December, it’s possible it will drag out longer. A6.4 SB is currently facilitating a series of public comment periods to receive feedback as to how they should structure their methodologies and certification standards.

Impact: Hard to say, perhaps a carbon market that is overseen by the UN will have greater ability to navigate the challenges that the existing voluntary carbon market and it’s standards have faced. There are major questions around what carbon credit types will be allowed, what methodologies will be used and how the market will interact with Nationally Determined Contributions.

Overlap/Opportunity: Many folks in the industry are looking at A6.4 with curiosity and a bit of confusion. It’s been a sort of black box ever since it was approved back in Paris in 2015. There are major questions around whether the Supervisory Body will seek to work with existing crediting programs and voluntary carbon market actors. I’m not sure exactly how they are approaching the design of the certification program for A6.4, but based on the public consultations, it seems like they are starting from ground zero.

This could go one of two ways. Creating a new certification program but involving the right stakeholders and building on the foundation of existing standards and market participants that is overseen by the UN could lead to the consolidation of standards and integrity initiatives that is respected by both governments and the private sector. But the key to achieving this is getting the right public and private sectors on board and well resourcing the Supervisory Body. OR A6.4SB could create an entirely new certification program that runs in parallel to existing programs and integrity initiatives and adds one more standard to a sector that already has too many standards. And, I worry that the UN is too bureaucratic to move fast enough and be efficient enough to allow this new system to get up and running quickly and be able to scale with the need.

My hope would be that A6.4SB is wise enough to work with current voluntary market and compliance market standards, registries and stakeholders to support convergence of the market, bringing resources and support together in one place, streamlining the crediting process and consolidating all the accounting (both at the level of governments and the private sector) under one roof.

And in terms of the implication for nature, technically the door is open to natural climate solutions, but they haven’t issued clarity on what project types would be included. According to a friend and expert in the space, Oliver Miltenberger, REDD credits will not be included in the A6.4. Stay tuned for a future post from me on the A6.4 Removals Consultation where we’ll take a deeper look at some of the implications for nature depending on how 6.4 gets operationalized.

Science Based Targets for Nature (SBTN)

Now let’s step beyond carbon and expand our frame to the other benefits of nature. What are the initiatives out there that could drive voluntary private sector action to protect and restore nature having nothing to do with carbon? Let’s start with the Science Based Targets for Nature.

Intention: SBTN builds on and complements SBTi’s Corporate Netzero Standard. The SBTN is a framework for companies to assess their environmental impacts and set nature related targets enabling companies to both reduce their negative impacts and increase positive ones for nature and people.

Status: SBTN has released their first version of guidance for certain steps and areas of targets (Freshwater and Land Use) and will be releasing more draft components (Biodiversity) over the next 6-12 months. Currently, 17 corporates are piloting the program.

Impact: The SBTN sets out for main target areas and provides guidance for corporates as to how to measure and report against those targets:

Freshwater

🔅 Target 1: Quantity - Set maximum allowable level of basin-wide withdrawals (water withdrawals corresponding to all water users in a given basin)

🔅 Target 2: Quality - the maximum allowable load of nutrients (Nitrogen and Phosphorus) for all nutrient sources in a basin and then define the portion of that amount of pollution (at the basin level) to be allocated to the company’s operations

Land Use

🔅 Target 1: No Conversion of Natural Ecosystems

🔅 Target 2: Land Footprint Reduction

🔅 Target 3: Landscape Engagement

Biodiversity

🔅 Targets to be defined - ensuring companies contribute to the protection, restoration and sustainable use of natural ecosystems

GHG emissions

🔅 Set a climate target via Science Based Targets initiative (SBTi)

Overlap: As it pertains to the climate mitigation initiatives described above, additionality is the big question in my mind. If SBTN gets up and going and driving corporate action to protect/restore ecosystems, how might that affect the additionality of nature-based carbon projects and vice/versa? How should we be thinking about financial additionality in particular when we are looking at nature restoration and conservation and multiple ecosystem services that might each be valued differently?

Fortunately, as you’ll see below, the TNFD is aiming to align with the corporate target-setting approach developed by the Science-Based Targets for Nature (SBTN)

Opportunity: The opportunity for TNFD and SBTN I see as largely one and the same, keep reading below for where I see them going.

Taskforce for Nature-related Financial Disclosures (TNFD)

Intention: As stated on their website, TNFD’s mission is “To develop and deliver a risk management and disclosure framework for organisations to report and act on evolving nature-related risks, with the ultimate aim of supporting a shift in global financial flows away from nature-negative outcomes and toward nature-positive outcomes.” The Taskforce consists of 40 individual Taskforce Members representing financial institutions, corporates and market service providers with over US$20t in assets.

TNFD builds on the Taskforce for Climate related Financial Disclosures (TCFD) and is essentially a framework for corporates and financial services firms to assess their dependencies and impacts on nature, and to identify nature-related risks and opportunities. My understanding is that the purpose of TNFD is both to assess the material impact that an entities activity have on nature as well as identify how the business of the entity itself is exposed to nature-related risk and how much they are contributing to opportunities to restore and protect ecosystems.

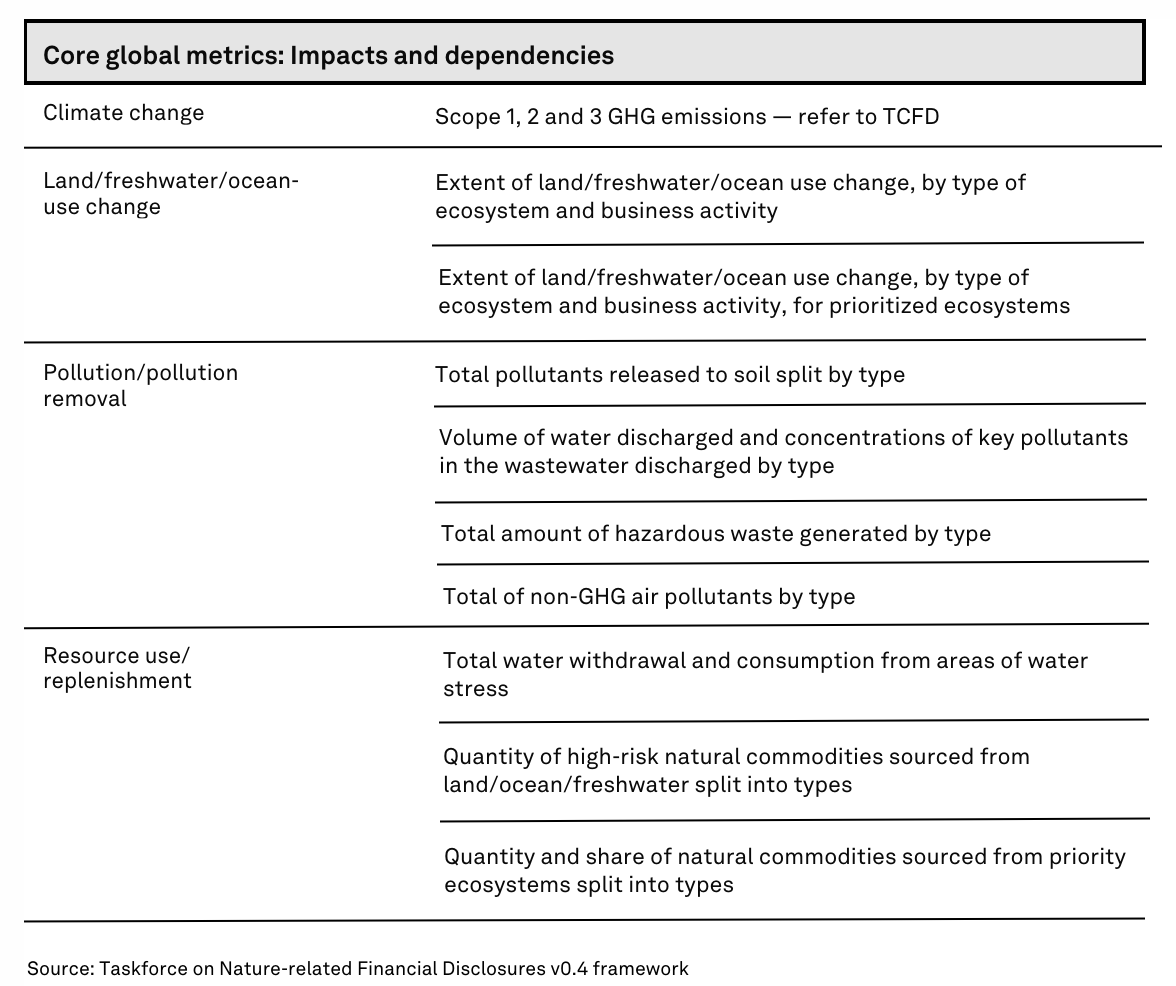

The core global metrics include 5 risk and opportunity metrics:

and 10 impact and dependency metrics:

Status: In March 2023, TNFD released the fourth version of its beta framework for market consultation. The release of version v1.0 of the full framework for market adoption will be in September 2023.

Impact and Opportunity: Just as the first step towards private sector climate action was to measure corporate emissions, the first step for TNFD is to measure the Risks, Opportunities, Impacts and Dependencies as it relates to nature. The key question is how does measurement translate to action and changes in business-as-usual.

The TNFD is currently engaging with international actors to develop nature-related targets at the global, national and local level to encourage coordinated action. The question is whether there will be a set of claims that corporates and financial managers can make to demonstrate their achievement of certain targets driving corporate voluntary action or whether governments can pass legislation that requires corporates to take action towards meeting these targets (regulation). My sense is that, just as we’ve seen with carbon and climate action, voluntary action and drivers will come first and hopefully that will transition to more regulation that can be legally enforced.

From what I’ve seen so far, measuring and reporting on these targets is likely going to be far more complex than carbon and the question is whether the targets can be simple enough for corporates to follow and yet complex enough to truly represent the value of biodiversity and ecosystem services. My guess is if TNFD starts to get traction with corporates, there will be a huge growth in demand for NatureTech services that can help measure and report on the targets.

We are a ways from TNFD having clear and defined targets for corporates to report against. The main focus currently is how do we measure overall corporate impact on the environment and nature-related risks to the business itself. Then we can start making progress towards target setting.

Overlap: Where does the initiative have overlap, whether in a good way or a bad way with other initiatives and what are the implications?

At the global level, the TNFD seeks to align with the environment-related Sustainable Development Goals and the post-2020 Global Biodiversity Framework. At the organizational level, the TNFD also seeks to align with the corporate target-setting approach developed by the Science-Based Targets for Nature (SBTN). As the SBTN is also currently developing their own set of targets, I truly hope that they work with TNFD to adopt the same targets and standards to give corporates clear guidance to follow and avoid confusion.

I also want to emphasize how critical it is to ensure that any nature-related targets can integrate into climate related targets and vice versa. As carbon sequestration is one of the key ecosystem services of nature, the value of that benefit should be considered alongside the value of other benefits. I can see some making an argument that if a forest restoration project was able to be financially viable with carbon revenues, then it isn’t additional financially for other ecosystem services. But this is a mistake and will just lead to us continuing to undervalue nature and undercompensate those for protecting and restoring ecosystems.

As nature becomes as much of a focus as climate for global action, it will be interesting to see whether natural continues to primarily serve carbon accounting purposes or whether the carbon sequestering ecosystem service of nature gets rolled into the other ecosystem services and biodiversity. My hope is that while nature itself becomes as important as climate outcomes, we continue to grow natural climate solutions within climate action and we transition over time to a system where all of nature’s benefits are living under one framework and the carbon sequestration component of that framework can plug into carbon accounting and climate mitigation claims.

But what is the structure that will drive nature-positive action, is it offsets, contributions, something else?

My hope for TNFD and SBTN is that the targets lead to corporates reducing their impact on nature, but as we’ve seen with climate, it won’t be enough to reduce emissions, we also need to remove carbon that is currently in the atmosphere to stabilize the climate. It isn’t enough for corporates to only reduce their impact on nature, we need to restore habitats to stabilize nature.

I don’t see nature markets following an offsets structure where you can destroy one area of land as long as you are restoring another, because we can’t afford to let any more natural ecosystems be destroyed. I do see nature markets being driven by corporates reducing their impact on nature within their supply chain, which will open up vast opportunities for restoration that should also be the financial responsibility of corporates and governments to undo the damage they have done. So if we use language from the climate mitigation world, instead of nature markets being based on an offsetting mechanism, I see them being structured around more of a contribution system after corporates have reduced their material impact (largely their land footprint).

I’ve also heard of a few folks looking at an NPV (Net Present Value) for land approach that incorporates biodiversity and ecosystem service value as a more efficient and effective way to achieve conservation and restoration rather than target setting and enforcement, but I’ll be the first one to admit that I’m not sure how exactly this would work/interact with initiatives like TNFD and SBTN. The Landbanking Group is one to keep an eye on that is doing quite a bit of work on this approach.

What’s next?

If you’ve made it this far, bravo! Hopefully you now have a bit more of an understanding of the state of the space for where carbon meets nature (and beyond).

Stay tuned for our next installment in the series where I plan to deep dive into Article 6.4 and specifically the Carbon Removal Consultation that is setting the rules and regulations for the creation and trading of removals credits under A6.4 (important to get these right for natural climate solutions to be included). I’ll be posting the next installment on LinkedIn, but feel free to subscribe to this substack and you’ll get an email when it’s released. I’ll be continuing to track and write about these initiatives and any other initiatives that come across my radar that have potential to drive private sector and government action towards protecting and restoring nature. And, change can come both top down and bottom up, I’m planning as well on sharing some case study examples that are leading the way for what’s possible for incorporating the value of nature into our economic and financial systems.

🌳 I highly recommend going for a 20 minute walk in nature to let the subconscious digest the above 🙂.

Big thanks to Oliver Miltenberger for feedback on the initial draft.

💭 All thoughts and feedback on my analysis and recommendations are most welcome via LinkedIn message or commenting on the post on LinkedIn.

And with that, I’ll leave you with my mantra for 2023:

We’re in the grey, and that’s ok.

Eric love your insights, please post more.

Very comprehensive and useful summary Eric. Well done! Big thank you